While significant updates to SBA lending guidelines may not be on the immediate horizon, the dynamic nature of the industry means that subtle shifts and evolving market conditions could influence the landscape in 2025. With a new SBA administrator set to take the reins this year, the direction of the Small Business Administration could change, possibly leading to fresh updates that could impact both lenders and borrowers.

That said, the SBA lending market remains strong, and there are several trends and insights that small business owners, lenders, and stakeholders should be aware of moving forward.

1. Strong SBA Loan Production Post-COVID, With Consistent Outlook Ahead

SBA loan production has remained resilient since the pandemic, with strong numbers across various loan programs. The steady appetite for SBA loans is expected to persist, as small business owners continue to seek financing to fuel growth and expansion. Historically, SBA originations have been consistent, even during economic downturns like the 2008 financial crisis. Given that backdrop, the SBA's loan programs remain a stable source of capital for small businesses in 2025.

The market outlook for small-business lending remains strong, with a special focus on small balance loans, particularly in the $100K to $500K range for existing businesses. This segment has seen growth in recent years, with more lenders offering flexibility and increased financing options. Small balance loans are often used for acquisitions, working capital, equipment purchases, and ownership changes. Furthermore, many lenders are now offering 100% financing options for qualified borrowers, providing an opportunity for businesses to grow with minimal upfront capital.

2. Shifting Lender Behavior: More Lenient and Aggressive with Caution

While lenders are showing more flexibility in the small balance space, there’s also a noticeable shift in behavior. Banks are becoming more aggressive in their lending approach, particularly in the sub-$500K loan segment. However, this is tempered with caution—lenders are focusing on maintaining a calculated level of risk. This reflects a more measured approach as lenders aim to secure the best possible outcomes without exposing themselves to unnecessary defaults.

A major part of this calculated risk is ensuring that businesses have a history of solid lending practices and underwriting. Defaults are on the rise, often linked to businesses that fail to meet these standards. Without solid financial practices in place, SBA guarantees won’t carry as much weight, and the risk of default increases. As a result, lenders are focused on ensuring that small business owners understand the expectations surrounding credit quality, financial history, and long-term viability.

3. New Dynamics in Bank Acquisitions and Credit Requirements

2025 also brings with it an interesting shift in the banking sector. With increasing consolidation and acquisitions in the banking world, banks are looking to grow through mergers and acquisitions. However, to facilitate this growth, they need clean balance sheets—something that could affect their willingness to lend aggressively. Banks must remain cautious about taking on additional risk, especially as they prepare to acquire other institutions.

This means that small business owners who rely on SBA loans will likely see more stringent credit quality requirements from banks, particularly when it comes to credit risk. While private equity investors often focus on the upside potential of a business, banks are more cautious and typically focus on the downside. This makes it crucial for businesses to demonstrate a well-managed financial profile and a solid business history.

4. Expectations Around Debt Service Coverage Ratios (DSCR)

The importance of a business’s Debt Service Coverage Ratio (DSCR) cannot be overstated in 2025. Banks and lenders typically require a minimum DSCR for SBA loans, meaning that a business must generate enough income to cover its debt obligations and maintain financial stability. If a business falls below this threshold, it may struggle to secure SBA funding.

For businesses that fall below the DSCR requirement, lenders will often turn to other financing options, such as private equity or other forms of funding, typically used by businesses already in operation or looking to buy out competitors. This approach focuses more on the upside potential of acquiring or expanding existing operations rather than building from scratch.

5. New Challenges and the Need for Experience in SBA Lending

With the growing complexity of the SBA lending process, it’s becoming increasingly important for both lenders and borrowers to have direct industry experience. Or have a partner in the deal with direct industry experience. SBA lenders expect small business owners to understand the nuances of their industry and the specific credit risk associated with their business type. Regardless of a borrower’s background, lenders will want to see that the applicant has a thorough understanding of the business landscape and a proven track record in their field.

This is particularly important in the small balance acquisition space, where transactions often involve businesses purchasing competitors or expanding into new markets. Lenders will not only look at the borrower’s financials but also at their history of working in the space, as businesses with no solid track record of industry experience may struggle to secure favorable loan terms.

6. Debt-to-Equity Ratio and SBA Lending

One of the key metrics lenders will continue to focus on is the Debt-to-Equity Ratio (D/E). A typical SBA guideline suggests maintaining a 9:1 ratio for businesses seeking SBA funding, though this may vary based on the specific loan type and the financial situation of the business. Maintaining a balanced D/E ratio is critical for ensuring the lender’s confidence in the borrower’s ability to manage debt responsibly.

Looking Ahead: A Strong Foundation for SBA Lending in 2025

In 2025, SBA lending remains a crucial avenue for small businesses to secure financing, with many lenders offering flexible options in the small balance space. While the landscape is shifting—driven by changes in bank acquisition strategies, the rise in defaults, and evolving credit quality expectations—SBA loans continue to provide stability for businesses looking to grow.

As the SBA’s new administrator takes charge, future changes in SBA guidelines may arise. However, for now, businesses seeking SBA loans in the small balance range should be prepared for more flexible lending terms and be aware of the increasing importance of solid financial practices and industry experience. The market outlook is strong, but the emphasis will remain on calculated risk and ensuring businesses are well-positioned for long-term success.

%20%20Process%2C%20Valuation%20%26%20Legal%20Checklist.png)

%20in%20a%20%2420M%20Sale..png)

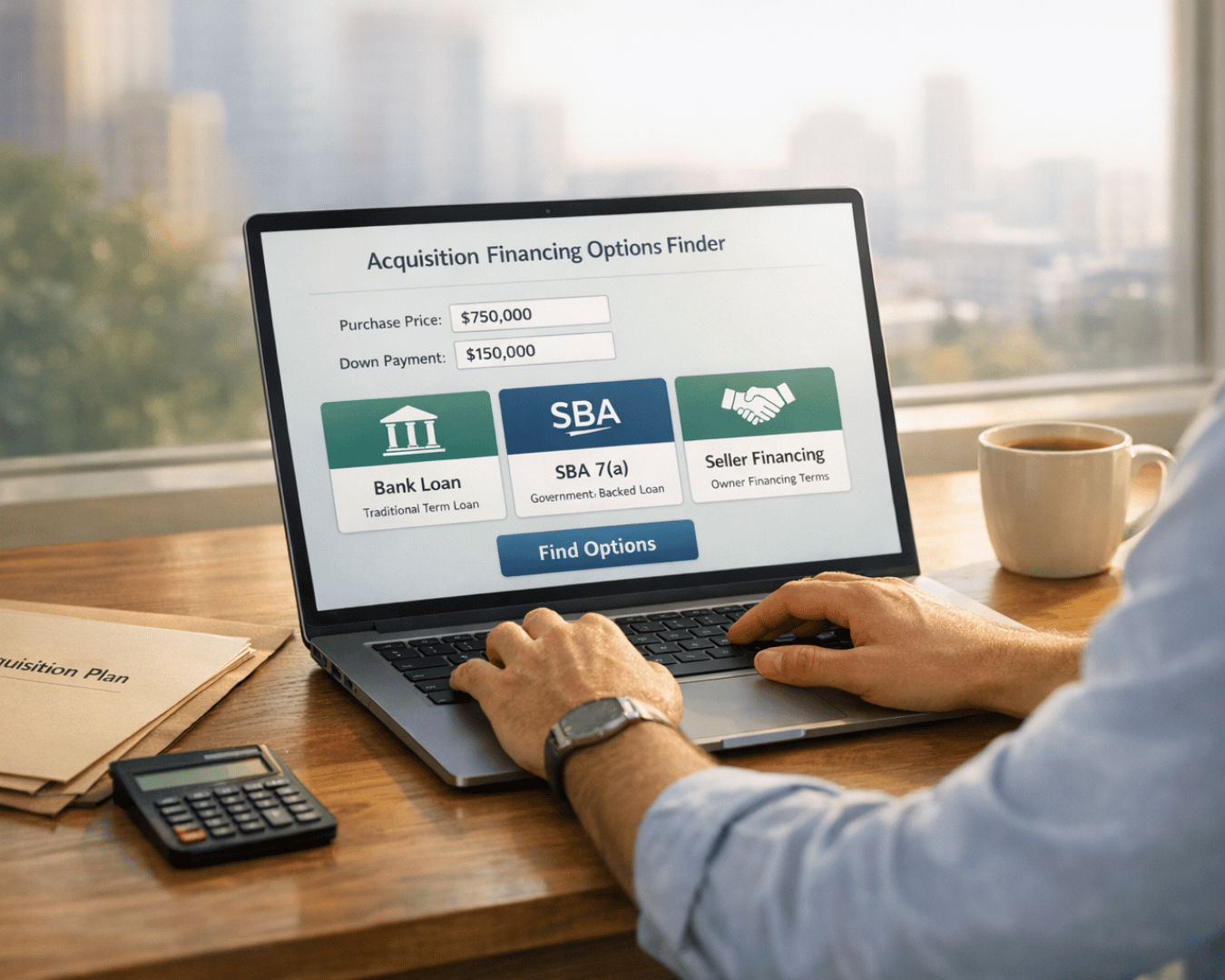

%20vs.%20Conventional%20Loans%20for%20business%20acquisition.png)

.png)

.png)

.png)